Performing short-term forecast of day-ahead electricity price is a daily activity for many energy operators. One of the most adopted technique is the so-called delta analysis, i.e., get yesterday bid&ask curves and properly shifting to take into account the forecast of renewable and consumption.

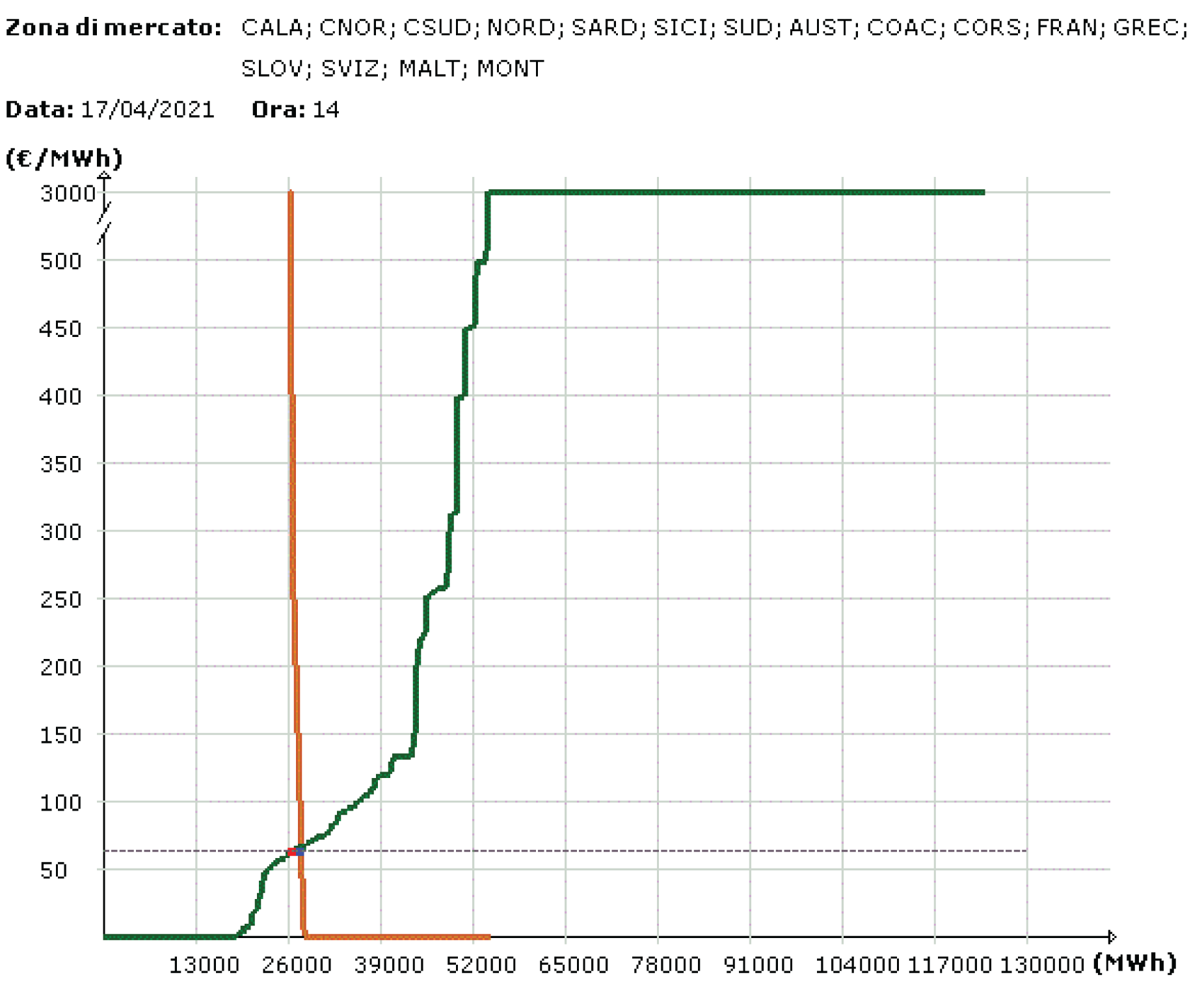

Considering the Italian market, it has seven different market zone linked with an ATC transmission model, with possibly seven different prices and the PUN. The GME publish every day the aggregated bid&ask curves as resulting of the SDMC algorithm. So, for instance, for the 17th April 2021 at 14 hours, the GME publish one couple of aggregated curves for all the Italy, even if each market zone has its own set of offers.

Aggregated curves of 17th April 2021 at 14 hours (Source GME)

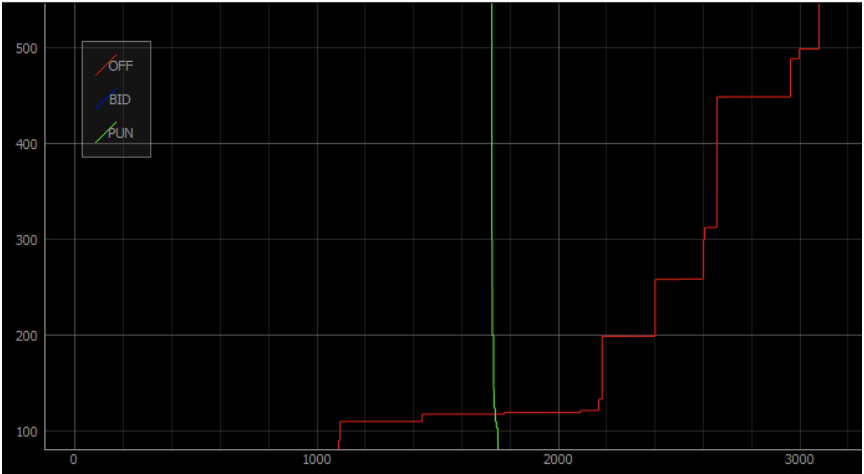

Biddings of SICI market area. (Source GME)

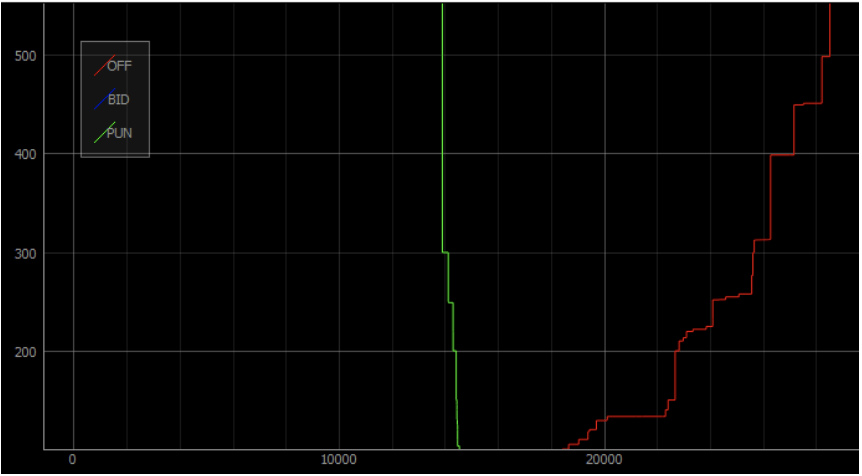

Biddings of NORD market area. (Source GME)

Is there an effective way to disaggregate the curves in order to guess the offers submitted to each market zone so to perform effectively the delta analysis? The short answer is yes. It is possible to write an optimal assignment problem in order to allocate the segments of the aggregated curves to a specific market zone, maximizing the likelihood of the zonal bids.

Such an algorithm is already implemented in PowerSchedO for PCR, the full-featured solution for the short-term electricity day-ahead market.